Everyone talks about scarcity and investment potential, but the real story lives in how these metals get used in the real world. The industrial demand profile tells you more about future price movements than any supply chart ever will.

When you look at a gold versus silver industrial uses chart, you’re examining fundamentally different economic animals.

Gold sits there like a quiet reserve asset, used sparingly in electronics but hoarded by central banks.

Silver behaves like a hyperactive commodity, powering solar panels, electronics, and industrial processes while somehow also trying to maintain investment credibility. The difference between these two creates opportunities and risks that most analyses completely miss.

Understanding the Demand Structure

Gold dedicates only 7-10% of its total demand to industrial applications, while silver commits a staggering 50-60% to industry. This fundamentally changes how each metal responds to economic conditions.

Think of gold as the tenured professor with a stable income. Whether the economy booms or crashes, central banks keep buying.

Jewelry demand stays relatively consistent across cultures.

Industrial users need those tiny amounts for semiconductors regardless of cost because there’s literally no substitute that won’t corrode. This creates price stability that silver simply cannot match.

Silver acts like a freelance contractor working three jobs simultaneously. It needs to satisfy industrial buyers who disappear during recessions, jewelry manufacturers competing on price, and investment demand that evaporates when stocks rally.

Each demand source pulls in different directions depending on economic conditions, creating that characteristic volatility that makes silver 1.5 to 2 times more volatile than gold.

The numbers from 2023 reveal silver’s demand composition clearly: Industrial applications consumed 48%, jewelry took 18%, investment accounted for 22%, silverware grabbed 5%, and photography’s ghost still claimed 3%. Gold’s breakdown looks completely different: Jewelry dominated at 47%, investment took 29%, central banks accumulated 23%, and technology consumed just 7%.

These structural differences mean comparing their “investment potential” without acknowledging their demand profiles misses the entire story. The composition of demand decides price behavior more than the total quantity demanded. A metal with diverse, stable demand sources will consistently outperform one with concentrated, cyclical demand during periods of uncertainty, regardless of which one seems “scarcer” on paper.

Electronics and Semiconductor Applications

Gold’s role in electronics centers on one irreplaceable characteristic: it doesn’t tarnish. Ever.

While silver conducts electricity slightly better, it reacts with sulfur compounds in the air to form a non-conductive layer that ruins electrical connections. This single chemical difference locked silver out of the most valuable electronics applications decades ago.

Every smartphone contains gold because bonding wires connecting chips to circuit boards must survive years of temperature cycling, humidity exposure, and chemical contamination. Gold provides that reliability at microscopic scale.

We’re talking milligrams per device, but multiplied across billions of units, it creates steady, price-inelastic demand.

When Apple designs a new iPhone, they can’t substitute copper and hope for the best. The failure rate would destroy their reputation.

The device might cost $1,000 to purchase, but the gold content costs maybe 50 cents.

At that ratio, manufacturers pay whatever gold costs because product reliability matters infinitely more than raw material savings.

This price inelasticity creates remarkable stability in gold’s electronics demand. During the 2008 financial crisis, while automotive and construction industries collapsed, semiconductor manufacturers kept ordering gold because their production schedules didn’t change and the cost represented such a tiny fraction of finished product value.

Silver dominates the high-volume, lower-reliability electronics sector. Solder joints, printed circuit boards, membrane switches, and basic electrical contacts use silver because conductivity matters more than corrosion resistance in these applications.

The protective coatings and sealed environments in modern electronics minimize tarnishing problems enough that silver works fine.

The semiconductor manufacturing sector illustrates this division perfectly. Gold appears in critical bonding applications where failure isn’t acceptable.

Silver shows up in bulk conductive applications where volume and cost drive decisions.

Neither can fully replace the other because their chemical properties create performance tradeoffs that engineering can’t overcome.

The electronics sector consumes roughly 280-300 tonnes of gold annually worldwide. That might sound like a lot, but it represents only about 7% of total gold demand.

Compare that to silver’s electronics consumption of about 250 million ounces annually, representing nearly 25% of total silver demand.

This concentration means electronics cycles hit silver prices hard while barely registering on gold’s demand profile.

The Solar Panel Revolution

Silver’s most dramatic industrial growth story centers on photovoltaic solar panels. Demand exploded from 50 million ounces in 2010 to 140 million ounces by 2023 as global solar capacity expanded exponentially.

Each solar cell needs silver paste to create electrical connections that carry current from the photovoltaic material to the collection system.

Here’s the counterintuitive twist that most precious metals analysts miss: manufacturers have been frantically reducing silver content per panel through a process called “thrifting.” Advanced paste formulations, precision application techniques, and improved cell designs have cut silver loadings per megawatt dramatically even as total capacity grows.

The 2024 data specifically notes “sharp reduction in silver loadings” achieved through “notable advancements within the PV segment.” This represents genuine engineering progress. When manufacturers can reduce silver content 20-30% while improving or maintaining efficiency, the scarcity narrative weakens considerably.

What does this mean practically? Solar capacity might double over the next decade, but silver demand might only increase 40-50% because each panel uses progressively less material.

This efficiency dynamic rarely appears in bullish silver analyses, but it represents a real headwind to industrial demand growth.

I’ve watched this pattern repeat across industries throughout my career analyzing commodities. Whenever a metal’s price rises significantly, engineers get creative about reducing consumption.

Copper wiring got thinner.

Platinum loadings in catalytic converters decreased. Gold bonding wires became finer. Material science always responds to price pressure, and silver in solar panels follows the same trajectory.

The renewable energy infrastructure beyond solar also consumes silver. Wind turbines, grid infrastructure, battery systems, and charging networks all need silver’s conductivity.

As countries pursue decarbonization policies, this creates a structural demand floor independent of economic cycles, supporting silver prices during recessions when other industrial demand collapses.

Medical and Antimicrobial Applications

Silver’s antibacterial properties have been recognized for thousands of years, but modern medicine has found increasingly sophisticated applications. Wound dressings impregnated with silver particles prevent infections in burn victims.

Catheters coated with silver compounds reduce hospital-acquired infections.

Water purification systems use silver to eliminate bacteria without harsh chemicals.

The emerging antimicrobial clothing sector represents a growth opportunity few traditional commodity analysts track. Athletic wear, medical scrubs, and even everyday garments increasingly incorporate silver-threaded fabrics that prevent bacterial growth and odor.

As healthcare-associated infection concerns rise globally, silver’s role in medical devices and hospital environments expands steadily.

Medical silver consumption currently represents a relatively small percentage of total demand, probably around 5-7% globally. However, this sector grows consistently regardless of economic cycles because healthcare spending proves remarkably recession-resistant.

When industrial buyers vanish during downturns, medical demand continues, providing some price support.

Gold’s medical applications differ fundamentally. Biocompatibility drives gold use as opposed to antimicrobial action.

Pacemakers use gold-plated contacts because the human body doesn’t reject or react to gold.

Specialized stents and implants incorporate gold when long-term chemical stability matters more than cost. Dental applications continue using gold alloys because they’re durable, workable, and biologically inert.

The medical sector consumes perhaps 10-15 tonnes of gold annually worldwide, representing well under 1% of total gold demand. This tiny exposure means medical applications barely register in gold market dynamics, unlike silver where medical use creates meaningful demand.

Platinum’s fastest-growing sector is actually medical applications. Platinum-based chemotherapy drugs like cisplatin treat various cancers.

Specialized surgical instruments and implants use platinum where both biocompatibility and extreme durability matter.

The emerging oncology applications create demand that operates independently of automotive or jewelry cycles, potentially stabilizing platinum’s notoriously volatile pricing.

Automotive and Catalytic Converter Dynamics

Platinum faces unique concentration risk: roughly 40% of all platinum mined annually goes into catalytic converters for automotive emissions control. This creates a direct link between platinum prices and global vehicle production that doesn’t exist for gold or silver.

The chemistry is remarkable and unforgiving. Platinum catalyzes the conversion of toxic carbon monoxide and nitrogen oxides into benign carbon dioxide and nitrogen at temperatures exceeding 600-900°C continuously.

No other material combination satisfies the thermal cycling requirements, chemical reactivity needs, and durability standards simultaneously.

Attempts to substitute cheaper palladium work in some applications but sacrifice efficiency and longevity.

This automotive dependency means platinum crashes during recessions when car sales collapse. In 2008-2009, platinum prices fell over 60% as automotive production ground to a halt.

Gold actually rose during that same period as safe-haven demand accelerated. This divergence illustrates why industrial dependency creates volatility as opposed to price support.

The long-term outlook for automotive platinum demand faces uncertainty from electric vehicle adoption. EVs don’t need catalytic converters because they don’t have combustion exhaust.

However, hybrid vehicles still need them, and the global vehicle fleet turns over slowly.

Catalytic converter demand likely stays substantial for decades even as EV market share grows.

Silver has minimal automotive exposure, primarily appearing in electrical systems and contacts. Gold essentially doesn’t appear in automotive applications at all.

This sector-specific risk concentration makes platinum behave more like an industrial commodity during recessions while gold maintains its safe-haven characteristics.

The Byproduct Problem

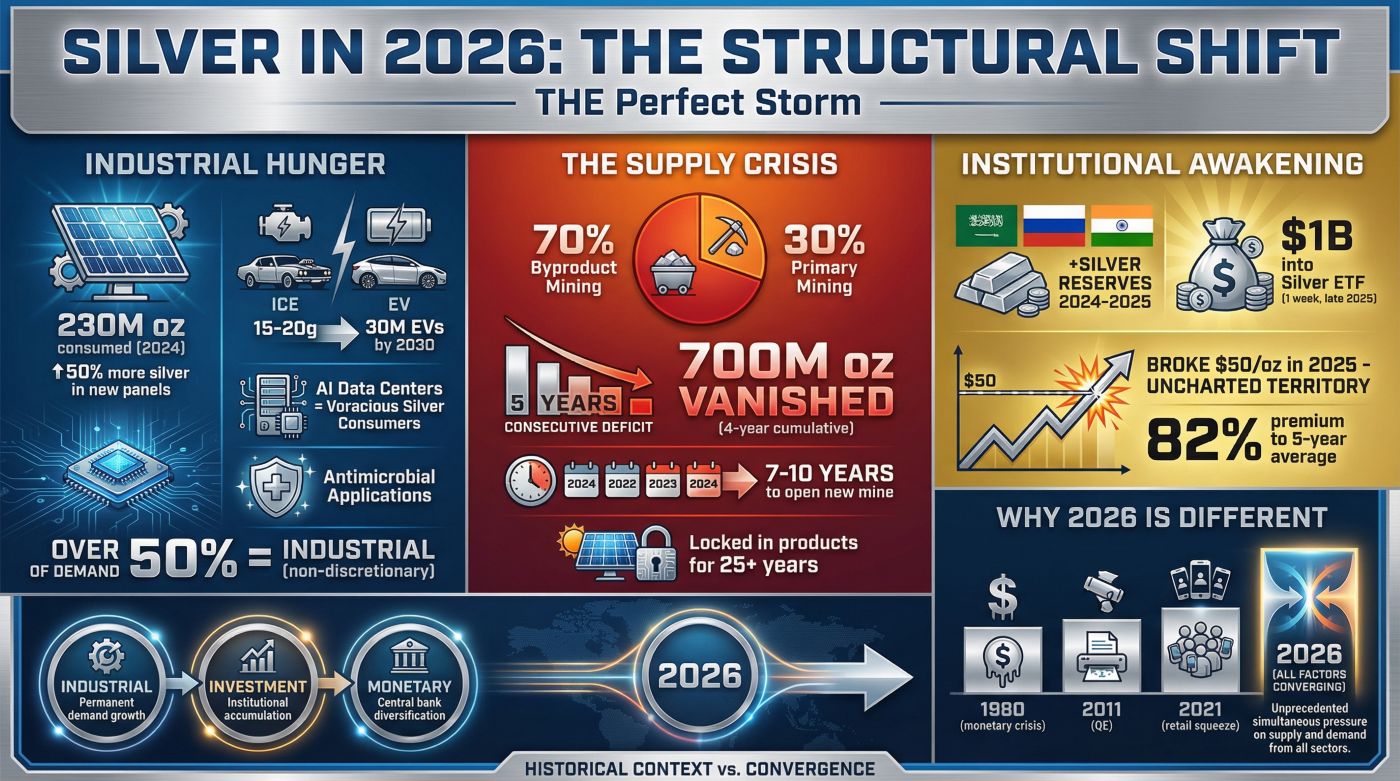

Silver faces a unique supply challenge that gold and platinum largely avoid: about 70% of silver comes as a byproduct of copper, lead, and zinc mining. This means silver supply can’t respond directly to silver prices.

When silver rallies, miners can’t simply increase silver production because they’d need to mine more base metals first.

The 2024 data illustrates this dynamic perfectly. Silver production from lead and zinc mines remained essentially flat while silver from gold mining operations surged 12% to a three-year high.

Silver supply responded to gold mining economics as opposed to silver prices, creating a supply response that’s disconnected from silver’s own market fundamentals.

This byproduct nature creates both opportunities and risks. During base metal booms, silver supply increases regardless of silver prices, potentially capping price appreciation.

During base metal busts, silver supply contracts even if silver prices are rising, potentially accelerating rallies.

The cascading effect through many mining sectors makes silver supply forecasting considerably more complex than gold supply analysis.

Gold production can be controlled more directly. Miners invest in gold-specific projects based on gold prices.

When gold rallies sustainably, new mines eventually come online, increasing supply with a 5-10 year lag.

This creates more predictable supply elasticity compared to silver’s byproduct-driven dynamics.

I’ve seen silver bulls get frustrated when silver prices rise but supply keeps increasing anyway because copper miners are responding to copper prices. The byproduct dynamic creates a supply ceiling that pure silver fundamentals can’t overcome, limiting how high prices can sustainably rise before extra supply floods the market.

The Recycling Relief Valve

Recycling surged in 2024 to reach a 12-year high of 193.9 million ounces for silver, climbing 6% year-over-year. This data point contradicts the common “we’re running out of silver” narrative that pervades precious metals discussions.

When prices rise sufficiently, secondary supply responds dramatically.

The composition of recycled silver reveals interesting economic patterns. Industrial scrap from electronics processing increased substantially as manufacturers recovered silver from production waste and obsolete equipment.

Silverware recycling jumped 11% as households liquidated family heirlooms under cost-of-living pressure.

This behavioral signal suggests economic stress that traditional indicators might miss entirely.

Gold recycling follows similar patterns but with different motivations. Jewelry recycling speeds up in developing nations when gold prices rally and households need cash.

Electronics recycling recovers gold from obsolete smartphones, computers, and telecommunications equipment.

The relatively higher value per unit makes gold recycling economically viable even for small-scale operations.

The ability of recycling to surge during price rallies creates a natural price ceiling that mining depletion analyses often ignore. If recycled supply can increase 10-20% within a single year, the “inevitable shortage” scenario becomes considerably less inevitable.

The market shows remarkable efficiency in recovering and reprocessing metals when prices justify the effort.

Platinum recycling primarily comes from spent automotive catalytic converters. Specialized processors recover platinum from scrapped vehicles, creating a secondary supply stream that responds to both platinum prices and vehicle scrappage rates.

During economic booms when people buy new cars, old vehicles get scrapped faster, increasing platinum recycling regardless of platinum prices.

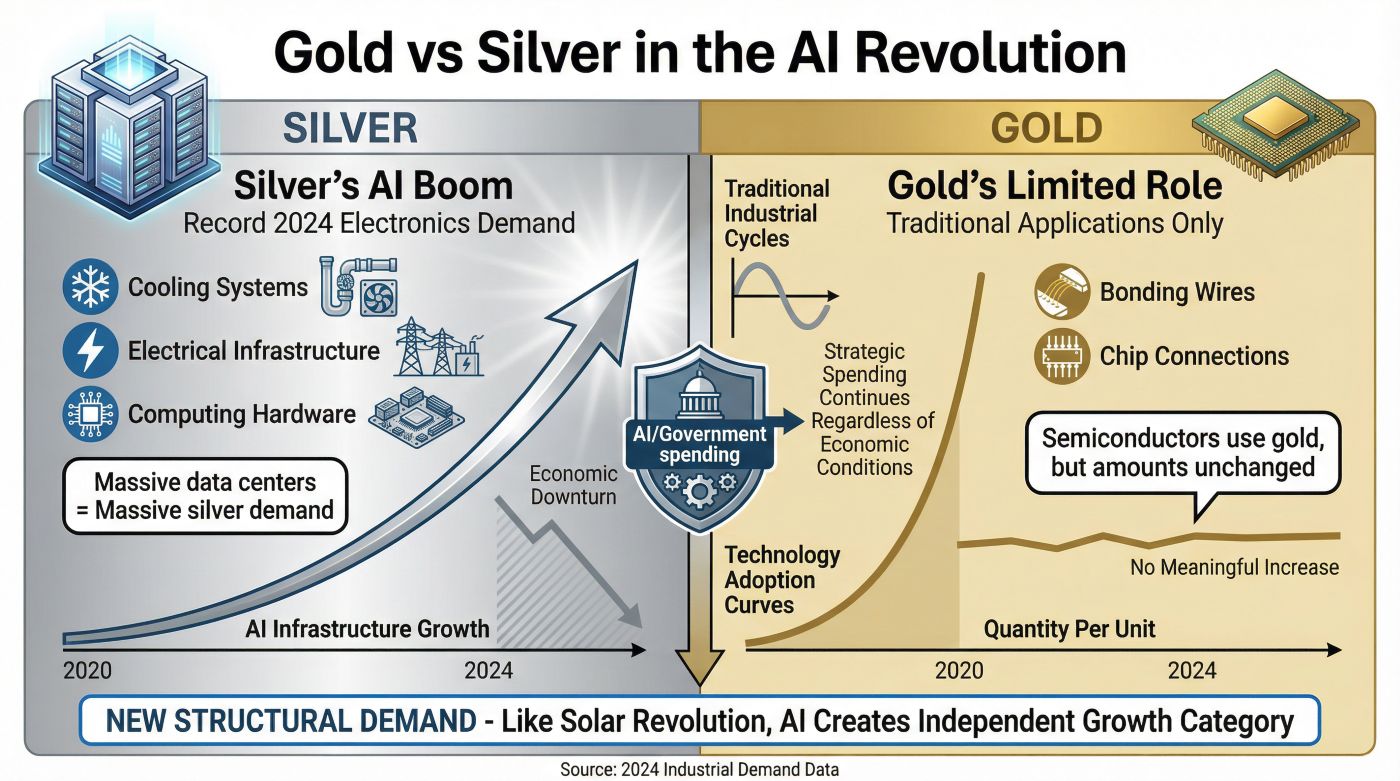

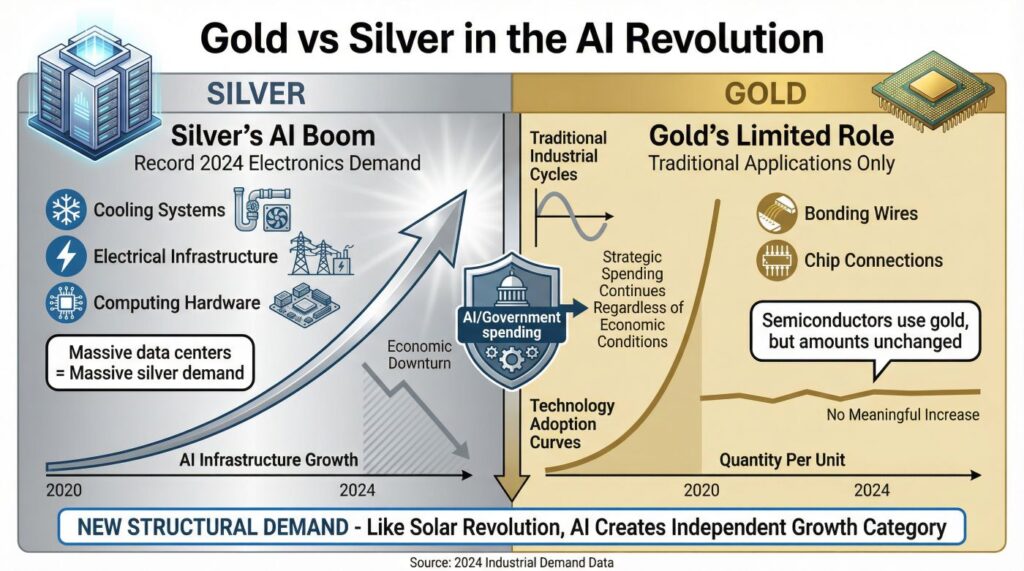

Emerging Demand: AI and Data Centers

The 2024 data specifically mentions “AI-related applications” driving record electronics and electrical demand for silver. As artificial intelligence infrastructure expands globally, the massive data centers required for training and operating AI models create sustained demand for silver in cooling systems, electrical infrastructure, and specialized computing hardware.

This emerging sector operates differently from traditional industrial cycles. AI infrastructure investment follows technology adoption curves as opposed to manufacturing cycles, potentially creating demand growth that persists even during economic downturns.

The strategic importance nations place on AI capabilities means government and corporate spending may continue regardless of broader economic conditions.

Gold’s role in AI infrastructure stays limited to traditional semiconductor applications. The servers and processors powering AI use gold bonding wires and connections, but the quantity per unit hasn’t increased meaningfully.

Silver benefits more directly from the physical infrastructure requirements of massive data centers.

This technological shift represents the kind of unexpected demand driver that traditional commodity analyses miss. Just as the solar revolution created a new demand category for silver, AI infrastructure may create another structural demand source that operates independently of established industrial cycles.

Key Investment Implications

The basic lesson from comparing industrial uses across precious metals centers on a counterintuitive reality: industrial demand creates volatility as opposed to price support. Platinum, despite being 30 times rarer than gold, trades at lower prices because its industrial concentration creates economic sensitivity that overwhelms rarity.

Silver’s extensive industrial demand means it amplifies economic cycles as opposed to providing protection from them. During expansions, silver often outperforms as both industrial and investment demand speed up simultaneously.

During contractions, silver falls alongside industrial commodities even as investment demand tries to provide support.

Gold’s minimal industrial exposure allows its safe-haven and monetary characteristics to dominate price behavior. Central banks accumulate regardless of economic conditions.

Jewelry demand stays relatively stable across cultures.

The small industrial component satisfies critical needs that persist through recessions. This demand structure creates price stability that silver and platinum cannot match.

The “thrifting” phenomenon represents a real headwind to industrial demand growth that bullish analyses often minimize. When solar manufacturers reduce silver content 20-30% per panel through engineering advances, sector growth no longer translates proportionally to metal demand growth.

Similarly, electronics miniaturization reduces gold content per device even as device production increases.

Recycling’s ability to surge dramatically during price rallies creates a supply response that conventional mining analyses miss. The 2024 recycling surge to a 12-year high shows that secondary supply can increase substantially within a single year, removing the “inevitable shortage” foundation from many precious metals investment theses.

Understanding that demand structure matters more than scarcity changes how you assess these metals as investments. The metal with the most stable, diversified demand sources tends to perform best during uncertainty regardless of how much exists underground or in applications.

Industrial utility doesn’t automatically translate to investment value, it often creates exactly the opposite effect.

Frequently Asked Questions

Does silver conduct electricity better than gold?

Yes, silver conducts electricity better than any other metal. However, gold dominates premium electronics applications because it doesn’t tarnish or corrode, providing superior long-term reliability despite slightly lower conductivity.

Why do solar panels use silver instead of cheaper metals?

Solar panels need silver’s exceptional electrical conductivity combined with workability in paste form. While manufacturers actively work to reduce silver content through engineering improvements, no current choice matches silver’s performance characteristics at similar cost.

How much silver is in a solar panel?

Modern solar panels contain about 10-20 grams of silver per panel, down significantly from earlier designs. Advanced manufacturing techniques continue reducing silver loadings while maintaining or improving efficiency.

Can platinum replace gold in electronics?

Platinum cannot effectively replace gold in most electronics applications. Gold’s combination of electrical conductivity, corrosion resistance, and workability at the microscopic scale required for semiconductor bonding stays unmatched by platinum.

What percentage of silver comes from dedicated silver mines?

Only about 30% of silver production comes from dedicated silver mines. The remaining 70% comes as a byproduct of copper, lead, zinc, and gold mining, meaning silver supply responds to base metal economics as opposed to silver prices alone.

Will electric vehicles reduce platinum demand?

Electric vehicles don’t need catalytic converters, which will eventually reduce platinum demand as EV market share grows. However, hybrid vehicles still need converters, and the global vehicle fleet replacement cycle spans decades, maintaining substantial platinum demand long-term.

How much gold is in a smartphone?

A typical smartphone contains about 0.034 grams of gold, primarily in bonding wires and connector contacts. While tiny per device, billions of units create significant aggregate demand for gold in electronics.

Does silver lose value from industrial use?

Silver used industrially often becomes difficult or uneconomical to recover, effectively removing it from available supply. However, high-grade industrial scrap and obsolete electronics do get recycled when prices justify recovery costs, as evidenced by 2024’s 12-year recycling high.